My Unified Theory of Real Estate Contracts

/Passle/65737bea961a63814fd9b845/SearchServiceImages/2025-09-16-21-03-42-834-68c9d0ae8206a7b639843f0f.jpg)

We transactional attorneys spend much of our time buried deep in the details of contracts, scrutinizing small edits to subclauses of lengthy sentences. Sometimes it is fun to step back and look at our work from a bird’s-eye view. While doing so, I have come up with what I call my “Unified Theory” of real estate contracts.

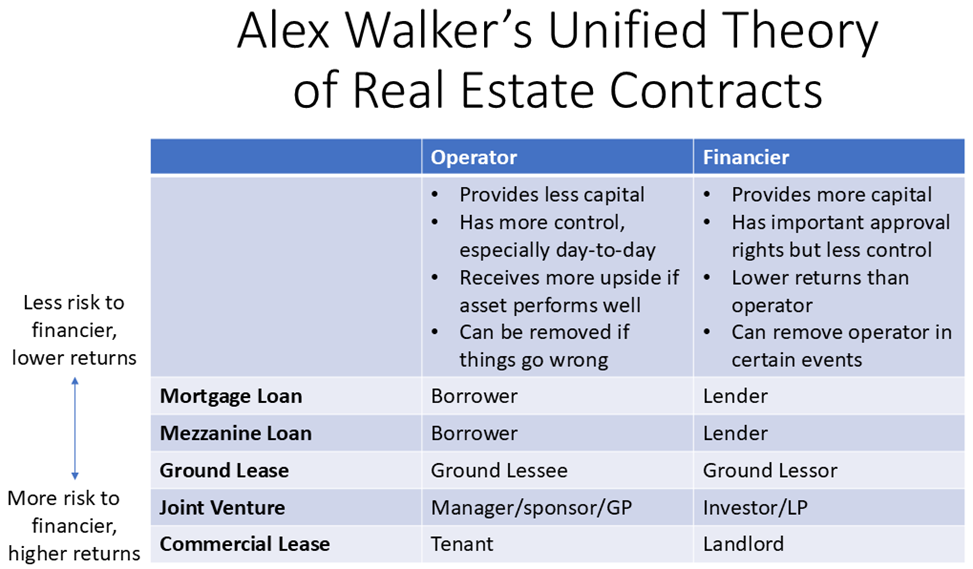

Here is my theory: many of the types of contracts that we, as real estate attorneys, see as distinct are actually quite similar. The most common form of real estate contract is one where two parties share “ownership” of some real estate asset, with one party providing a larger share of the required capital and the other party providing less. The party providing less capital has greater control over the real estate asset, especially in the day-to-day operations, and takes more of the upside if the asset performs well. The party providing more capital has a safer position and generally gets its money back first or at a higher priority in the capital stack. The party providing capital also has some important approval rights over the operation of the real estate asset, and is able to remove the other party from control, and potentially the capital stack, if things go sideways.

The description above most closely resembles a typical real estate joint venture, but if you think about it, it also covers mortgages, mezzanine loans, and ground leases. On one side is the joint venture manager, borrower, or ground lessee, providing less capital but holding more control and taking more upside. For simplicity, I will call these parties the “operator.” On the other side is the joint venture investor, lender, or ground lessor, providing more capital and holding important approval rights, but generally ceding day-to-day operations. I will call these parties the “financier.”

The primary way that these contracts differ is in the amount of risk that the financier takes, which is reflected in the amount of return that the financier expects in exchange for taking that risk. In bankruptcy, broadly speaking, a party with secured debt (like a mortgage or mezzanine lender) is the most likely to recover some or all of their funds, and debt is paid before equity owners receive anything. As a result, a mortgage lender takes the least risk, with the lowest returns (and these returns are not based on the property’s performance but rather a pre-determined rate). A mezzanine lender takes a bit more risk and expects a higher return. A ground lessor takes on more risk than a lender, while a joint venture investor takes on the most risk, receiving higher returns tied to the performance of the property. A joint venture investor is also more closely involved in the operation of the real estate asset than a lender, often approving annual budgets and other more granular details of operations at the property.

As real estate professionals know, many deals involve two or more of these contracts (creating a “capital stack”), and some of the most complex negotiations are between the different financiers regarding their respective approval rights and remedies, with the operator acting as a go-between, trying to preserve their own rights and make everyone get along. For example, a mortgage lender will not want a joint venture investor to kick out the joint venture manager and replace them with someone the lender has not approved. Similarly, a mortgage lender who lends to a ground lessee will want the right to cure any defaults of the ground lessee under the ground lease, to protect their collateral, and may bargain for time to foreclose on the borrower’s interest in the ground lease before the ground lessor can terminate the ground lease. In addition, one party can be an operator in some aspects of the deal and a financier in other aspects. For example, a ground lessor can borrow a mortgage loan.

Leases for retail, office, and industrial space have similarities to the form of contract described above, but with an important distinction: the tenant uses the real estate for the purposes of their own business, rather than operating the real estate as a financial asset. But the tenant still has more day-to-day control over the real estate, takes on more risk and upside (in the income from their business) than the landlord takes, and can be removed for violating the lease.

I hope you have enjoyed this exercise in looking at these contracts at a higher level. I am sure that I am not the first person to see these commonalities, but I have not seen anyone else put all of the pieces together. Below is a diagram that summarizes my Unified Theory.

/Passle/65737bea961a63814fd9b845/SearchServiceImages/2025-10-08-23-19-47-904-68e6f193a2228e83d76216f2.jpg)

/Passle/65737bea961a63814fd9b845/SearchServiceImages/2025-10-24-22-37-35-202-68fbffafe660a4c38e3ed5d4.jpg)